Kerr Financial Group

Kildare Asset Mgt.

Jeffrey J. Kerr, CFA

Newsletter

November 29, 2021 – DJIA = 34,899 – S&P 500 = 4,594– Nasdaq = 15,491

December Distractions

With Thanksgiving behind us, it’s a furious rush to Christmas and the New Years. Everyone will be checking their list and probably more than twice. Adding to the typical seasonal madness this year is a nonstop news flow of covid variants, possible shutdowns, destructive inflation, supply chain shortages, and intense cultural division. It’s enough to distract the most devoted traders from what’s going on in the markets. It could also divert individual investors from considering possible tax saving year-end strategies.

Acknowledging that our readers are no less harried, we’ll briefly offer some thoughts on both the markets and tax strategies. First, some tax reduction steps. Maxing out retirement plans contributions such as 401Ks, IRAs, and similar plans can be done in December. This reduces taxable income or provides a deduction on your taxes.

Secondly, funding a Health Savings Account (HSA) is a way of reducing taxes. HSA’s are open to individuals with high deductible health plans (HDHP) and contributions to the HSA are tax deductible. The 2021 contribution limits are $3,600 for an individual and $7,200 for a family. HSA’s are open to a wide part of the population but are underutilized.

Finally, tax loss harvesting involves selling investment positions that are showing a loss. Net losses up to $3,000 per year are deductible on your tax return. The trades have to done before December 31, 2021, in order to qualify for 2021 taxes. Contact us if you need more information or have questions concerning any of these strategies.

Concerning the markets, we began the week after experiencing a painful plunge on Friday. It was the worst day of 2021 for the Dow Jones Industrial Averages as it tumbled 900 points. Thankfully, the markets were only open half day for the Thanksgiving weekend.

This “Black Friday” in the markets was triggered by worries over a new covid strain in South Africa. Fears of economic shutdowns grew as the Biden administration announced the start of travel bans from South Africa and 7 other countries. Of course, the losses were widespread as the S&P 500 and Nasdaq’s drops were similar the Dow’s.

While the over 2% declines for the major averages were unpleasant, three trading days prior saw fresh all-time highs for the S&P 500 and Nasdaq Composite. At the end of last week, the major averages still showed strong year-to-date gains. Here is the year-to-date performance for the major averages as of November 26.

As gloomy as Friday was, there are reasons to think it is not a replay of the March 2020 drop on the initial shutdown. First, there are signs of economic growth. Mortgage applications have been increasing and manufacturing PMI (purchase manager activity) was greater in November than October. Finally, personal income increased and came in higher than forecast.

To be sure the economy is far from healthy and we all know some worrisome signals. However, there are some signals that stocks could trade higher in the short term. First, there are rumors that many hedge funds, traders, and institutions are underperforming the markets. With one month left, they will likely have to add exposure to narrow the gap. If this is accurate, it could provide a floor for prices.

Next, last week’s selling could have marked an inflection point. The VIX has reached levels that have coincided with previous market bottoms. First, the VIX is an index derived from options on the S&P 500. It is intended to gauge trader sentiment with higher numbers meaning greater fear.

The VIX recently moved above the 30 level. Hedgeye Risk Management reports that this might be an important stock market bottom. According to Hedgeye[i],

· Over the last decade, the VIX has breached 30 exactly 9 times

· If you had bought the VIX when it breached 30, you would have made money 8 out of 9 times over the next 30 days

· The average gain was +6% for the SP500 over those periods

· The only time this batting average didn’t hold was in March 2020.

Here is a chart comparing the VIX to the S&P 500 during the past decade. As can be seen, the VIX spends a lot of time trading in the teens. Also, we can see the performance after the 9 instances of trading above 30. Of course, there are several similarities with the March 2020 (the one time where the S&P 500 fell after a VIX above 30) and now. It could easily result in a 2 out of 10 outcome.

In the sprint to the end of the year that many of us will be caught in, it will be easy to take our eye off the capital markets. And perhaps this is good – a kind of Hanukkah or Christmas gift. Nevertheless, some will want to look at some tax saving strategies as well as trading opportunities. Contact me if we can help you.

[i] Hedgeye “Early Look”, December 3, 2021

Copy of the 4th Quarter Review Letter

/0 Comments/in Financial Planning News /by jkerrKERR FINANCIAL GROUP

KILDARE ASSET MANAGEMENT

45 Lewis Street, Lackawanna RR Station

Binghamton, NY 13901

Phone: 607-231-6330 email: [email protected]

The following is a copy of the 2021 4th quarter letter sent to clients. It reviews the markets and the client account’s activity and performance for the 4th quarter of 2021.

February 10, 2022

The S&P 500 has had three consecutive years of double-digit gains. It was up 27% in 2021. Given the challenges and turmoil that we have endured, this is a remarkable outcome. These three-peats of double-digit returns have only happened 9 times in the history of the index. The last time was 2012 – 2014 as the economy was recovering from the Great Financial Crisis.

Looking at the year-end numbers, one could naturally assume it was all unicorns and rainbows. In other words, every decision was a good one and trading profits abounded. This is not what happened. The year began with the controversies surrounding the meme stocks (GameStop, AMC, etc.) and the Robinhood gang.

These stocks rocketed early in the year as individual investors targeted companies high short interest positions which caused pain and consternation throughout Wall Street. The established old guard of the financial industry fought back, and some trading platforms restricted “buy” orders in the meme stocks. Eventually, the battle calmed a bit and many of the stocks returned to their previous levels.

Another development of 2021 was the growth and popularity of SPACs (special purpose acquisition company). These organizations raised money from selling stock and then used that money to buy another company that had, unlike the SPAC, business operations. There was a high level of excitement and speculation around SPACs and their potential targets. The price of many SPACs dropped in the second half of 2021.

Commodities prices captured some headlines. Lumber futures began the year below $1,000 per 111,000 per board feet (one 73-foot railcar). The price jumped to $1,700 and then plunged to $500 before ending the year above $1,100.

Bitcoin had a similar roller coaster trip. It started the year around $37,500 and reached $60,000. It plummeted 50% and then recovered to above $47,000 at year end. As with the meme stocks and lumber, if you bought bitcoin or another cryptocurrency at the wrong time it was a regretful decision.

Back in the stock market there were rotations between industries and sectors which offered rewards to those navigated these changes. It was a challenging trip for those who may have been a step behind.

For example, the Russell 2000 (small cap index) was the best performing of the major indexes in the first 6 months (+17%). The Russell lost 2.8% in the second half of the year. Most of this drop came in November and December as the index peaked on November 8th. The Nasdaq also peaked in November and drifted sideways into year end.

Despite all the gyrations, it was a good year the stock markets. The S&P 500 logged 70 all-time highs during the year. Here are the major indexes’ performance numbers for the 4th quarter and for the entire year.

In 2021, the markets overlooked and overcame such obstacles as inflation, covid variants, widespread shortages of goods, intense cultural division, and geopolitical tensions. Those probably continue in 2022 and then could be compounded with other headwinds. The biggest of the new issues could come from interest rate increases by the Federal Reserve.

The Fed is projecting that they will raise interest rates at least four times this year. Our monetary officials are targeting inflation and believe that the economic momentum is strong enough absorb this reversal in monetary strategy. The first-rate hike is expected to be in March.

There is widespread confidence that the Federal Reserve can successfully raise interest rates without inflicting damage. An extension of this is that Wall Street thinks the Fed has its back and won’t let the stock market fall. This has developed over the past decade as the Fed has implemented multiple versions of quantitative easing which primarily supported the capital markets.

The current trust in the Fed might be misplaced as our central bankers, unfortunately, have s a long history of blunders. As an example, the Fed told us for many years that they would generate a 2% inflation rate. Until last year’s spike in prices, they failed.

Another policy misstep happened in 2018. The Fed attempted to cut back on stimulus (bond purchases) and raise interest rates. As the Fed acted the stock market fell. When it became clear that the Fed was going to keep tightening, stocks collapsed. The S&P 500 lost 20% in the 4th quarter of 2018. In early January 2019, Fed Chairman Powell ‘pivoted’ and announced the interest rates increases would end. The stock markets stabilized and started to move higher.

I worry that 2022 could be a replay of 2018. The Fed is strongly committed to multiple interest rate increases this year. Currently, the markets appear to be understanding. I fear that there could be significant harm as interest rates go up while inflation remains elevated, and growth slows. As a reminder, this would be within an overleveraged financial system which increases risk.

The capital markets have a lot of factors to deal with under normal conditions. This year will present an even greater number of issues for the economy to understand and digest. This could result in a step up in volatility. This landscape could be tricky but will likely present many opportunities.

Please contact me with questions or comments. As always, thank you for your support and confidence in Kerr Financial Group.

Sincerely,

Jeffrey J. Kerr, CFA

President

Global Tensions and Risks to the Market

/0 Comments/in Financial Planning News /by jkerrA Fed driven nor’easter targets Wall Street

/0 Comments/in Financial Planning News /by jkerrCopy of the 3rd Quarter Review Letter

/0 Comments/in Financial Planning News /by jkerrKERR FINANCIAL GROUP

KILDARE ASSET MANAGEMENT

45 Lewis Street, Lackawanna RR Station

Binghamton, NY 13901 | Phone: 607-231-6330 | email: [email protected]

The following is a copy of the 2021 3rd quarter letter sent to clients. It reviews the markets and the client account’s activity and performance for the 3rd quarter of 2021.

November 3, 2021

In the past 40 years, inflation became an accepted part of our economy. This is partially a result of it being at low levels and not an obstacle to economic progress. After the financial crisis, inflation became an encouraged outcome of monetary policy. Our government and monetary bureaucrats have been telling us for the past decade that a “little” inflation is good thing. The Federal Reserve repeatedly told us they were working hard to achieve higher inflation levels.

While we were being sold that we needed inflation, we were also assured that that our leaders could manage all negative developments if any arose. What was absent in promotion of inflation is who it hurts. Inflation does the most damage on the middle and low classes as well as retirees on a fixed income. At the same time, the elites and wealthy feel little pain from the increases in gasoline, groceries, and the necessities of everyday life.

P.T. Barnum reportedly claimed that “Many people are gullible, and we can expect this to continue.” The modern public’s acceptance of such propaganda as a little inflation is good is evidence of the showman’s wisdom. The public’s unwillingness to hold leaders accountable for inflicting harmful policies and running up astounding amounts of debt is a head scratcher.

Inflation has soared in 2021. As measured by CPI (Consumer Price Index), the inflation rate was 1.4% in January 2021 and rose to 5% in May and has been above 5% for every month since. Government officials tell us it is transitory and will fall when the economy reopens. This is also the same gang that told they were working hard to get the inflation rate to 2% but couldn’t do it. Here is a chart of the recent monthly CPI readings.

Despite the claims that it is temporary, inflation could easily turn into a long-term issue. Labor shortages and supply chain disruptions will contribute to keeping prices higher. This could become circular in that businesses raise prices to cover higher costs and payrolls which causes other businesses along the food chain to do the same.

Concerning the markets, inflation has moved to the forefront of corporate mindsets. Few executives and managers have any history of decision making during high inflation environments which increases the possibility of bad ones. Nevertheless, rising prices is a clear corporate worry. The number of times that “inflation” was mentioned on 2nd quarter S&P 500 earnings conference calls jumped 900% year-over-year. Here is the chart.

How the financial markets cope with inflation could cause important variations from recent years. Increasing prices should hurt long maturity bonds which many investors think is “safe”. Further some industries will be challenged in passing along their higher costs. If shortages continue, some sectors will be able to command their price. It promises to be a different investing world.

Looking back at the 3rd quarter, the stock market finished flat to down. Despite just being a sideways slither, it was the worst quarterly stock market performance since 1st quarter 2020 (the Covid shutdown). The S&P 500, Dow Jones Industrial Average, and Nasdaq Composite climbed during July and August but gave back the quarter’s gains in September. For the year-to-date, all the averages are showing gains. Here are the major indexes’ performance number for the 3rd quarter and 2021.

The markets could be facing a classic case of be careful of what you wish for because you may get it. Our elected and unelected leaders have been telling us for years that the economy needs inflation. Until 2021, they couldn’t provide any lift in prices. Now that inflation has arrived, we are supposed to believe it is temporary. The Federal Reserve has a long history of being wrong so it would be prudent for investors to consider that inflation is a longer-term problem.

This new landscape will present new risks and opportunities. I will continue to take advantage of the favorable situations in this environment.

As a new part of this quarterly communication, we are attaching a video. I try to cover some specific positions and get into more detail on the how the markets have impacted your account. Please let me know any comments, questions, or suggestions.

As always, thank you for your support and confidence in Kerr Financial Group.

Sincerely,

Jeffery J. Kerr, CFA

“Why Can’t We Be Friends?”

/0 Comments/in Financial Planning News /by jkerrDecember Distractions

/0 Comments/in Financial Planning News /by jkerrKerr Financial Group

Kildare Asset Mgt.

Jeffrey J. Kerr, CFA

Newsletter

November 29, 2021 – DJIA = 34,899 – S&P 500 = 4,594– Nasdaq = 15,491

December Distractions

With Thanksgiving behind us, it’s a furious rush to Christmas and the New Years. Everyone will be checking their list and probably more than twice. Adding to the typical seasonal madness this year is a nonstop news flow of covid variants, possible shutdowns, destructive inflation, supply chain shortages, and intense cultural division. It’s enough to distract the most devoted traders from what’s going on in the markets. It could also divert individual investors from considering possible tax saving year-end strategies.

Acknowledging that our readers are no less harried, we’ll briefly offer some thoughts on both the markets and tax strategies. First, some tax reduction steps. Maxing out retirement plans contributions such as 401Ks, IRAs, and similar plans can be done in December. This reduces taxable income or provides a deduction on your taxes.

Secondly, funding a Health Savings Account (HSA) is a way of reducing taxes. HSA’s are open to individuals with high deductible health plans (HDHP) and contributions to the HSA are tax deductible. The 2021 contribution limits are $3,600 for an individual and $7,200 for a family. HSA’s are open to a wide part of the population but are underutilized.

Finally, tax loss harvesting involves selling investment positions that are showing a loss. Net losses up to $3,000 per year are deductible on your tax return. The trades have to done before December 31, 2021, in order to qualify for 2021 taxes. Contact us if you need more information or have questions concerning any of these strategies.

Concerning the markets, we began the week after experiencing a painful plunge on Friday. It was the worst day of 2021 for the Dow Jones Industrial Averages as it tumbled 900 points. Thankfully, the markets were only open half day for the Thanksgiving weekend.

This “Black Friday” in the markets was triggered by worries over a new covid strain in South Africa. Fears of economic shutdowns grew as the Biden administration announced the start of travel bans from South Africa and 7 other countries. Of course, the losses were widespread as the S&P 500 and Nasdaq’s drops were similar the Dow’s.

While the over 2% declines for the major averages were unpleasant, three trading days prior saw fresh all-time highs for the S&P 500 and Nasdaq Composite. At the end of last week, the major averages still showed strong year-to-date gains. Here is the year-to-date performance for the major averages as of November 26.

As gloomy as Friday was, there are reasons to think it is not a replay of the March 2020 drop on the initial shutdown. First, there are signs of economic growth. Mortgage applications have been increasing and manufacturing PMI (purchase manager activity) was greater in November than October. Finally, personal income increased and came in higher than forecast.

To be sure the economy is far from healthy and we all know some worrisome signals. However, there are some signals that stocks could trade higher in the short term. First, there are rumors that many hedge funds, traders, and institutions are underperforming the markets. With one month left, they will likely have to add exposure to narrow the gap. If this is accurate, it could provide a floor for prices.

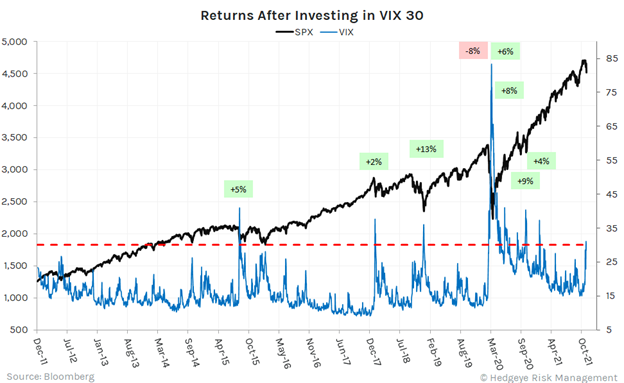

Next, last week’s selling could have marked an inflection point. The VIX has reached levels that have coincided with previous market bottoms. First, the VIX is an index derived from options on the S&P 500. It is intended to gauge trader sentiment with higher numbers meaning greater fear.

The VIX recently moved above the 30 level. Hedgeye Risk Management reports that this might be an important stock market bottom. According to Hedgeye[i],

· Over the last decade, the VIX has breached 30 exactly 9 times

· If you had bought the VIX when it breached 30, you would have made money 8 out of 9 times over the next 30 days

· The average gain was +6% for the SP500 over those periods

· The only time this batting average didn’t hold was in March 2020.

Here is a chart comparing the VIX to the S&P 500 during the past decade. As can be seen, the VIX spends a lot of time trading in the teens. Also, we can see the performance after the 9 instances of trading above 30. Of course, there are several similarities with the March 2020 (the one time where the S&P 500 fell after a VIX above 30) and now. It could easily result in a 2 out of 10 outcome.

In the sprint to the end of the year that many of us will be caught in, it will be easy to take our eye off the capital markets. And perhaps this is good – a kind of Hanukkah or Christmas gift. Nevertheless, some will want to look at some tax saving strategies as well as trading opportunities. Contact me if we can help you.

[i] Hedgeye “Early Look”, December 3, 2021

“I’d Love to Change the World”

/0 Comments/in Financial Planning News /by jkerrKerr Financial Group

Kildare Asset Mgt.

Jeffrey J. Kerr, CFA

Newsletter

October 25, 2021 – DJIA = 35,677 – S&P 500 = 4,544– Nasdaq = 15,090

“I’d Love to Change the World”[i]

The financial markets are accustomed to dealing with a lot of changes. Change is in every nook and cranny of the markets as our dynamic economy constantly offers new opportunities. In addition to these normal market transformations, there are recent changes that have been different and much more dramatic, and investors need to understand them.

Let’s take a closer look at three critical areas that are undergoing historic upheaval that can have big impacts on the markets. First interest rates are going up. A year ago, the 10-year Treasury bond’s yield was around ½%. This rate is now 1.67% and this is up from 1.25% in September.

The reason that this is important is that interest rates have been going down for 40 years. Obviously, 40 years is a long time. As expected with such a lengthy history, the global economic system has become addicted to low interest rates. Any change, let alone an increase, could be problematic. If interest rates keep moving higher it will be an obstacle that few business executives and investors have faced and are not likely to handle well.

What could be the reasons for the spike in rates? Record government deficits, that look to be growing even larger, will need to be financed in bond market. Investors could easily demand a better return (higher yield) with this large increase in bond issuance. Further, higher inflation (more on that below) will force rates higher. This is an environment that few have experienced so how the financial system reacts is unknown and could cause further problems if bad decisions are made.

Another turbulent development is the shortage of goods. Supply chain complications and labor issues have helped produce widespread delays and scarcity of things like appliances, electronics, cars, as well as commodities like copper, lumber, and iron ore. This is a drastic change in an economy that has excelled at innovation and delivery of goods and services often at lower cost.

Worker shortage is a big part of this issue. A record 4.3 million workers quit their job in August. This represents 2.9% of our workforce. It’s hard to believe that the labor shortage is cured if millions of people are leaving the workforce.

But in addition to the labor problems, the capacity to supply the materials needed for goods and products could be limited. This is a result of lower capital investment for things like energy, commodities, and materials. Annual spending by mining companies (copper, lead, zinc, etc.) is forecast to be 30% or more below the 2012 peak.

Energy exploration is seeing a more dramatic cutback. Analysts expect a small increase in capital investment, but it will likely remain below 2019’s levels and 40% – 50% below 2014’s record amount.

Investors are watching these events as the global economy reopens. The increased demand for commodities and energy is taking place at a time when the supply might be limited. This is impacting the markets through increased demand in alternative things that are available. The price of coal is up over 200% this year as power plants switch from using natural gas to coal to produce electricity. Maybe electric vehicles aren’t as clean as they proclaim.

Here are two graphs that reflect the projected investments for the energy and mining industries as published in The Wall Street Journal (September 24, 2021). Despite higher prices that would encourage increased production, ESG initiatives appear to be influencing this reduction.

Naturally, higher energy and commodity prices are feeding into the inflation measurements. Once again this is something we haven’t seen in decades. Prices are spiking in everything from necessities such as gasoline, food, electricity, heat, and rent. This is also seen in the industrial areas of the economy – higher transportation costs, higher raw materials, and higher labor costs.

The optimistic view is that these issues are temporary. We are told by bureaucrats and politicians that once the economy opens these troubles will be fixed. They tell us that we have to get past the pandemic, and everything will return to normal.

The changes in interest rates, goods and material shortages, and inflation represent a new economic landscape. Furthermore, the forces behind these developments are closely linked. The conventional wisdom is that this is all temporary and will go away. This could turn into a dangerous mindset if the obstacles facing economy are not easily resolved and become long term problems. It would be a new world with a different set of risks as well as opportunities. Feel free to contact us to hear the specifics on how we are handling these changes.

1 Alvin Lee, 1971

Copy of the 2nd Quarter Review Letter

/0 Comments/in Financial Planning News /by jkerrKERR FINANCIAL GROUP

KILDARE ASSET MANAGEMENT

45 Lewis Street, Lackawanna RR Station

Binghamton, NY 13901

Phone: 607-231-6330 email: [email protected]

The following is a copy of the 2021 2nd quarter letter sent to clients. It reviews the markets and the client account’s activity and performance for the 2nd quarter of 2021.

August 10, 2021

Wall Street is always introducing new products to trade and new ways to trade them. 2021 has provided both with the rise of SPACs and the Robinhood app. SPAC stands for Special Purpose Acquisition Company. It is a company that sells shares of their stock to raise money that is then used to buy another company. These target companies are usually a private organization.

SPACs became very popular in the first half of the year, and they generated a lot of speculation. The SPACs often disclosed their target company which led to investors bidding up the SPACs based on excitement and projections on the target company’s potential. The enthusiasm around these stocks isn’t as great as past bubbles but it was certainly a big part of the first half of 2021.

Another noteworthy financial market development is the battle between individual investors and the Wall Street establishment. The skirmish began when some investors connected by an online chatroom named “Wall Street Bets” targeted stocks that were heavily shorted by Wall Street including many hedge funds.

The “Robinhoodies” (one of the nicknames of the group of individual investors because they often used the Robinhood app to do trades) targeted the stocks of GameStop, AMC Entertainment, and Blackberry. Their buying pushed these stocks higher – GameStop’s stock spiked from under $20 per share to over $480 in two weeks. This resulted in heavy losses for some firms that had shorted the stocks (short positions look for falling stock prices to be profitable).

Wall Street fought back by restricting buy orders on the stocks. After a few days the friction decreased, and full trading access was restored. However, the battle between the Army of the Apes (another nickname for the individual investors) and established Wall Street is far from over. This could continue to influence trading in certain stocks and potentially impair other over leveraged Wall Street firms.

While I am normally skeptical on investing fads and gimmicks, not all of them are bad and some present opportunities. MP Materials Corporation (symbol MP) is a good example. MP came public after the operations were acquired by the SPAC Fortress Value Acquisition Corporation (symbol FVAC).

MP Materials is the owner and operator of Mountain Pass, the only rare earth mine and processing site in North America. Rare earth elements are important parts in industries such as manufacturing, technology, and defense. They are also required for many clean energy applications.

MP was included your account in the 4th quarter of 2020. Purchases of FVAC were before the merger (de-SPAC) and the entry price was in the low to mid-teens. After the deal was closed, the MP stock spiked to $40 in December and closed 2020 at $32. MP’s stock price has been volatile in 2021. It traded above $50 in the 1st quarter and then was cut in half in May. The stock rebounded and closed the quarter in the high $30’s.

MP’s volatility is partially a function of size as it is a small company and operations are growing. Further mining is a high-cost industry with steeper break-even metrics from other businesses. Finally, rare earth elements have a geopolitical component as China is the largest exporter of rare earths. This could be an advantage during tense international relationships. Despite the over 100% profits, I think MP’s stock price could continue to move higher over time as the importance of their mined elements grow.

Looking at the market in total, stocks had a good first half of 2021. The Russell 2000 Index which is a small cap index led the way. The Nasdaq Composite did some catching up in the 2nd quarter after lagging the other indexes in the 1st quarter. Here are the major indexes’ performance numbers for the 2nd quarter and the year-to-date.

As noted, the stock market leadership changed during the 2nd quarter. In addition to the shift from small cap to large cap, and low quality (SPACs and highly leveraged companies) to better balance sheets and higher quality, investors seem to be shifting to sectors that can succeed in inflationary times. This includes industries that can pass along their higher input costs and maintain their margins.

Technology and energy are two areas of the market that have historically done well in this environment. Commodities and the industries that supply them are another sector. Value and defensive stocks have lagged in inflationary times.

The fixed income market saw a steepening of the yield curve as inflation expectations have risen. This typically helps financial companies who normally rely on the spread between longer dated interest rates and short-term rates (they invest long-term at higher rates and borrow short-term at lower rates, taking advantage of the spread).

The current investment landscape is facing many unknowns. Uncertainty surrounding Covid and a delayed reopening could be a large economic hurdle. Continued shutdowns will squash any recovery. Societal division and widespread cultural acrimony are further massive challenges.

In the glass half full bin, the world is slowly reopening. Furthermore, history is full of examples of pandemics and dramatic shocks that resulted in an explosion of demand as the recovery takes hold – the millennial reference is YOLO or You Only Live Once. This path will result in a higher growth trajectory with expanding opportunities.

As we journey through the rest of 2021, I will look to balance these cross currents and take advantage of opportunities. I will focus on the changing risks to the system as well as individual securities.

Thank you for your support and confidence in Kerr Financial Group. Please contact me with any questions or comments.

Sincerely,

Jeffrey J. Kerr, CFA

“For It’s One, Two, Three Strikes You’re Out at The Old Ball Game”

/0 Comments/in Financial Planning News /by jkerr“For It’s One, Two, Three Strikes You’re Out at The Old Ball Game”

Kerr Financial Group

Kildare Asset Mgt.

Jeffrey J. Kerr, CFA

Newsletter

September 24, 2021 – DJIA = 34,764 – S&P 500 = 4,448– Nasdaq = 15,052

As October approaches many baseball fans are eagerly anticipating the World Series. The Fall Classic has a rich history with many memorable moments. “The Catch”, Don Larson’s perfect game, Bill Mazerorski’s walk off home run, the 1986 Mets, and Mr. October.

Of course, October brings a different type of anticipation as anxious investors tremble as they face the month with a tumultuous history. Also, there is increased intensity this year as the markets are facing some difficult pitches. On top of the normal fastballs, sliders and curveballs, investors are battling some nasty changeups and even some screwballs.

One of the trickier pitches is the signal from the 10-year treasury bond vs. the record levels of the stock market. In a normal world, stocks climb in a strengthening economy. Yet the 10-year t-note’s yield has fallen in recent months which is a sign of slowing conditions and decreasing demand for capital. Let’s look at the lineup of the opposing forces.

First, let’s review some statistics. The S&P 500 has had over 50 record closes in 2021 with the most recent on September 2nd. At the same time, the yield on the treasury bond has fallen from 1.75% in late March to current level around 1.30%.

So, let’s look at the two lineups that support these conflicts. First, the economy continues to improve which is supportive of equities. GDP is expanding and corporate earnings are rebounding. Further inflation can help stocks especially those industries that can pass along their higher costs in the form of price increases.

On the side of the treasury market being right, the August employment report was a big swing and miss by the economy. The data showed solid job growth, but the number was far below forecasts. Economists are now concerned that the job market may not recover as fast as previously expected.

Another headwind is a drop in consumer sentiment. The University of Michigan survey showed a decrease in consumer’s outlook. This is likely tied to the fact that 41% of households receive some form of government assistance. A weak and fearful consumer is not normally associated with a strong economy.

These mixed messages could spark some interesting market dynamics in the 4th quarter. Underperforming investors will be looking for any opportunity to regain lost ground. This could force buying which would offer a backstop for stocks and bonds. If buying begets buying, there could be a material move higher in the final three months of 2021.

All the major averages have declined in September. If the 10-year Treasury is correct, this might continue. However, this week we have bounced back from Monday’s Evergrande panic which might point to a short-term bottom for the equity market. Here is the year-to-date performance for the major averages as of September 23.

The change of seasons is upon us which will be quickly followed by the holiday season. Before we get there, October could give investors some curveballs along with some ghosts and goblins. It will be an interesting end to an interesting year.

“Very Superstitious, Writing’s on the Wall”

/0 Comments/in Financial Planning News /by jkerr