KERR FINANCIAL GROUP

KILDARE ASSET MANAGEMENT

45 Lewis Street, Lackawanna RR Station

Binghamton, NY 13901

Phone: 607-231-6330 email: [email protected]

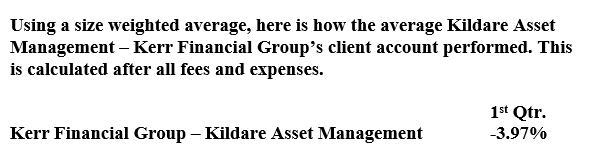

The following is a copy of the 2023 1st quarter letter sent to clients. It reviews the markets and the client account’s activity and performance for the 1st quarter of 2023.

May 24, 2023

Economic and monetary conditions have a big influence on the capital markets. It is easier for businesses to grow sales and profits when the economy is expanding together with monetary conditions that are not restrictive. Of course, growing revenues and net income support higher stock prices and a stronger bond market.

2022 was an historic example of a negative backdrop causing market turmoil. It was an unusual time where both stock and bonds declined together. There were many headwinds last year, but the main sources of the chaos were extraordinary inflation and aggressive interest rate increases.

In the middle of 2022, the year-over-year inflation rate exceeded 9% which is the highest rate in over 40 years. Disruptions in the supply chain caused shortages and higher prices across many markets. Inflation spread throughout the economy and it impacted consumers’ spending. The higher cost of necessities meant less was left over for discretionary items.

For corporations, higher costs and less revenue reduced corporate profits. This challenged those companies that were previously profitable and crushed speculative areas that were losing money.

Prior to 2022, interest rates had been declining for a generation. The Federal Reserve’s shift to a tighter monetary policy was implemented to battle the accelerating inflation. As was the case with rising prices, corporate managements had limited or no experience facing higher interest rates. It was a challenging landscape that upset the financial markets.

These market dynamics remained in place to start 2023. In addition to inflation and the Fed continuing to raise interest rates, the markets had to deal with increasing geopolitical tensions, even wider social division, and bank failures. It appeared that the news was getting worse.

Despite a deteriorating landscape, the financial markets stabilized throughout the first quarter. The fixed income market stopped going down and stocks strengthened. Markets often trade illogically, especially in the short term, but with some further investigation, possible explanations can be found.

The narrative associated with the financial markets’ first quarter touched many parts of 2022’s issues. From a broad view, the bulls believed that all the bad news had been priced in. It was assumed that the news flow would not be getting worse, and, if all damage from interest rates and inflation was discounted, the market might be ok.

An extension of this is that, if all the bad news had been discounted, the recession would be shallow, and inflation would be transitory. And once inflation is fixed, the Fed can stop raising interest rates, start cutting rates, and a strong recovery will begin. This is a big part of what drove the markets in the 1st quarter.

In addition to this storyline and as prices started to rally, there was another development that contributed to momentum. Daily expiring options in the SPY (S&P 500 ETF) and QQQ (Nasdaq 100 ETF) became a big part of the trading activity in the first quarter.

These options are referred to as 0DTE which stands for “0 days to expiration”. Traders and institutions are the big players in this strategy, and it developed into an influential part of trading in 2023. While this is an extremely short-term approach, it takes place every day and can have an outsized impact. Through a relatively small amount of capital, the option buyer can potentially manipulate the markets. This was not the only reason that stocks traded better but it played a role.

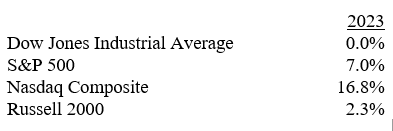

While the major averages were positive for the 1st quarter, the leadership was very select. Apple and Microsoft accounted for 40% of the S&P 500’s return in the quarter. Further, seven stocks drove the Nasdaq which was the best performer.

Here are the major indexes’ performance numbers for the 1st quarter.

Within your accounts, there are positions that hedge market risk. These performed well in 2022 as they helped manage risk. They were a significant drag in the 1st quarter as stocks rallied. It was compounded as our bullish positions did not move higher with the indexes. The narrowness of the rally meant that it was critical to have exposure to the few stocks that drove the move and that was not the case.

It is noteworthy that the economic problems that disrupted the markets in 2022 continue. The Fed has raised rates further in 2023. Inflation has fallen from last July’s reading but has remained higher than the Fed’s goal. Also, new risks have arisen in 2023. Silicon Valley Bank and two other banks have failed. This brings added stresses on the economy and financial system. There are signs that the troubles in the banking system continue.

The economy and markets are facing historic obstacles which present unique risks. Additionally, there is a lot of uncertainty in how to address these problems which could bring many unintended consequences. The bottom line is that the systemic turmoil of 2022 could return. Accordingly, risk management remains important. At some point opportunities will arise, but the timing is unclear.

Please contact me with questions or comments. I’m happy to explain what I think is going on within these volatile conditions. As always, thank you for your support and confidence in Kerr Financial Group.

Sincerely,

Jeffrey J. Kerr, CFA

President

Kerr Financial Group

A Look at the Labor Market

/0 Comments/in Financial Planning News /by jkerrhe job market and employment data are closely watched by the capital markets. There are many dynamics in the statistics but such things as the unemployment rate, level and trend of wages, and the labor participation rate get a lot of Wall Street’s attention.

The labor market is impacted by many things including monetary policy and the economic cycle. Additionally, recent cultural and technological changes have altered the employee-employer relationship, where people work, and the type of jobs demanded.

Here is a labor industry review which touches on some of these key issues.

Workforce Trends

It’s important to note that employers in 2023 are moving away from in-person wellness benefits, such as onsite seminars and provider meetings, toward more affordable, convenient, and scalable virtual options for employers and employees.

Labor Market Challenges

Regulatory Environment

Emerging Technologies

The employment market is undergoing many changes and hopefully this provides some insight. Please let us know any questions or comments.

Copy of the 1st Quarter Review Letter

/0 Comments/in Financial Planning News /by jkerrKERR FINANCIAL GROUP

KILDARE ASSET MANAGEMENT

45 Lewis Street, Lackawanna RR Station

Binghamton, NY 13901

Phone: 607-231-6330 email: [email protected]

The following is a copy of the 2023 1st quarter letter sent to clients. It reviews the markets and the client account’s activity and performance for the 1st quarter of 2023.

May 24, 2023

Economic and monetary conditions have a big influence on the capital markets. It is easier for businesses to grow sales and profits when the economy is expanding together with monetary conditions that are not restrictive. Of course, growing revenues and net income support higher stock prices and a stronger bond market.

2022 was an historic example of a negative backdrop causing market turmoil. It was an unusual time where both stock and bonds declined together. There were many headwinds last year, but the main sources of the chaos were extraordinary inflation and aggressive interest rate increases.

In the middle of 2022, the year-over-year inflation rate exceeded 9% which is the highest rate in over 40 years. Disruptions in the supply chain caused shortages and higher prices across many markets. Inflation spread throughout the economy and it impacted consumers’ spending. The higher cost of necessities meant less was left over for discretionary items.

For corporations, higher costs and less revenue reduced corporate profits. This challenged those companies that were previously profitable and crushed speculative areas that were losing money.

Prior to 2022, interest rates had been declining for a generation. The Federal Reserve’s shift to a tighter monetary policy was implemented to battle the accelerating inflation. As was the case with rising prices, corporate managements had limited or no experience facing higher interest rates. It was a challenging landscape that upset the financial markets.

These market dynamics remained in place to start 2023. In addition to inflation and the Fed continuing to raise interest rates, the markets had to deal with increasing geopolitical tensions, even wider social division, and bank failures. It appeared that the news was getting worse.

Despite a deteriorating landscape, the financial markets stabilized throughout the first quarter. The fixed income market stopped going down and stocks strengthened. Markets often trade illogically, especially in the short term, but with some further investigation, possible explanations can be found.

The narrative associated with the financial markets’ first quarter touched many parts of 2022’s issues. From a broad view, the bulls believed that all the bad news had been priced in. It was assumed that the news flow would not be getting worse, and, if all damage from interest rates and inflation was discounted, the market might be ok.

An extension of this is that, if all the bad news had been discounted, the recession would be shallow, and inflation would be transitory. And once inflation is fixed, the Fed can stop raising interest rates, start cutting rates, and a strong recovery will begin. This is a big part of what drove the markets in the 1st quarter.

In addition to this storyline and as prices started to rally, there was another development that contributed to momentum. Daily expiring options in the SPY (S&P 500 ETF) and QQQ (Nasdaq 100 ETF) became a big part of the trading activity in the first quarter.

These options are referred to as 0DTE which stands for “0 days to expiration”. Traders and institutions are the big players in this strategy, and it developed into an influential part of trading in 2023. While this is an extremely short-term approach, it takes place every day and can have an outsized impact. Through a relatively small amount of capital, the option buyer can potentially manipulate the markets. This was not the only reason that stocks traded better but it played a role.

While the major averages were positive for the 1st quarter, the leadership was very select. Apple and Microsoft accounted for 40% of the S&P 500’s return in the quarter. Further, seven stocks drove the Nasdaq which was the best performer.

Here are the major indexes’ performance numbers for the 1st quarter.

Within your accounts, there are positions that hedge market risk. These performed well in 2022 as they helped manage risk. They were a significant drag in the 1st quarter as stocks rallied. It was compounded as our bullish positions did not move higher with the indexes. The narrowness of the rally meant that it was critical to have exposure to the few stocks that drove the move and that was not the case.

It is noteworthy that the economic problems that disrupted the markets in 2022 continue. The Fed has raised rates further in 2023. Inflation has fallen from last July’s reading but has remained higher than the Fed’s goal. Also, new risks have arisen in 2023. Silicon Valley Bank and two other banks have failed. This brings added stresses on the economy and financial system. There are signs that the troubles in the banking system continue.

The economy and markets are facing historic obstacles which present unique risks. Additionally, there is a lot of uncertainty in how to address these problems which could bring many unintended consequences. The bottom line is that the systemic turmoil of 2022 could return. Accordingly, risk management remains important. At some point opportunities will arise, but the timing is unclear.

Please contact me with questions or comments. I’m happy to explain what I think is going on within these volatile conditions. As always, thank you for your support and confidence in Kerr Financial Group.

Sincerely,

Jeffrey J. Kerr, CFA

President

Kerr Financial Group

The S&P 493 – Not The Place To Be

/0 Comments/in Financial Planning News /by jkerrTraders’ Attention Spans Get Shorter – 0DTE Options

/0 Comments/in Financial Planning News /by jkerrKerr Financial Group

Kildare Asset Mgt.

Jeffrey J. Kerr, CFA

Newsletter

May 15, 2023 – DJIA = 33,300 – S&P 500 = 4,124 – Nasdaq = 12,284

“Traders’ Attention Spans Get Shorter – 0DTE Options”

There are many days where the financial markets seem to be light-years apart from economic reality. We have all scratched our heads on days when stocks rally after a terrible news report. Similarly, an upbeat report hits the wire and there is widespread turmoil across the markets. While this has been a common occurrence over the years, it has become more common because of new derivative and option trading strategies.

Daily options on the SPY and QQQ ETFs began trading in the second half of 2022 and have quickly grown to have a large role in the stock market. Before exploring this trading strategy, let’s provide some definitions. Put and call options can be a little confusing but basically buying a call option is bullish while buying a put option is bearish.

A call option offers the right but not obligation to buy an underlying security at a specific price any time before the call’s expiration. A put option is the right but not obligation to sell the underlying security at a specific price before the put’s expiration.

Here is a specific example using Apple (symbol = AAPL). The AAPL options expire every week. Looking at a call option that expires on June 16 with a strike price (the exercise price) of $180 per share. This means that the owner of the call option can buy Apple at $180 any time before June 16.

Obviously when Apple’s share price is trading around the current level of $172, the owner of the call will not exercise (buy at $180). But if Apple trades above $180 before June 16, the call owner can buy AAPL at $180.

Turning to the put side, the buyer of a $165 AAPL put option with the same expiration date (June 16th) provides the right to sell AAPL shares at $165 before Jun 16. It wouldn’t make sense if Apple is trading in the $170’s, but if AAPL has fallen to the low $160’s, then put holders will gladly sell Apple shares at the higher price ($165).

To complicate the situation further, the price of these options trade and move up and down according to the stock price relative to the exercise price and the amount of time left before expiration.

With this Introduction, we move the focus to the recent development of daily expiring options. While many large stocks and the major indexes began offering options that expired each week, the SPY and QQQ started trading options in 2022 that expire every day. The SPY and QQQ are ETFs that mirror the S&P 500 and Nasdaq 100 indexes, and these are the securities on which the daily options trade.

These daily options are referred to as “0DTE” which stands for Zero Days to Expiration. In other words, these options expire at the end of the current trading day. The pricing of these options is entirely based on the S&P 500 and Nasdaq 100’s intraday price movements. Obviously, given the limited shelf life, this is for nimble traders who can react and adjust quickly.

The growth of 0DTE trading has been massive and led to some unexpected market influences. From a high-level view, when 0DTE options are bought (a bullish strategy), the dealer who sells these options now has added risk. The dealer had essentially sold short the options which means they are at risk of rising prices (they will lose money if stock rally).

Logically, dealers hedge their risk from the selling of call options by buying the underlying stocks of the index or they buy futures options on the index. This buying of stocks and futures pushes prices higher which then encourages more 0DTE call buying which forces more stock and futures buying. This can easily turn into a circular exercise which can move stock prices regardless of the news flow.

There is evidence that this was a big part of the stock market’s trading in the 1st quarter of 2023. The S&P 500 was up over 7% in the first quarter and the Nasdaq Composite rose almost 17%. This happened within an environment where banks failed, inflation remained high, the Federal Reserve raised interest rates, and the economic data weakened.

0DTE trading is being used as a short-term trading tactic and has very little correlation to the fundamental economic data. Traders, who are undoubtedly aware of the problems that are challenging the economy, believe they can rapidly adapt their positions to a changing stock market through this strategy.

The trading of 0DTE options has changed the way the stock markets move in the short term. To be sure, the circular machinations have helped stock prices in 2023. However, this can work in reverse if stock prices begin to drop. It could cause a rapid and steep drop if put option buying starts to outweigh the call buying. Dealers would have to hedge against declining prices and a dive could accelerate.

This is a complicated subject which can be confusing. Please feel free to call or email me and I’ll try to answer and explain further. One of the main conclusions from the growth of 0DTE is that underlying risks get masked in the short term. Ignoring risks doesn’t mean that they are reduced or eliminated. In fact, it could result in greater risks as financial asset prices move further away from reality. This could be the story of 2023.

Wall Street Asks If The Glass Is Half Full

/0 Comments/in Financial Planning News /by jkerrKerr Financial Group

Kildare Asset Mgt.

Jeffrey J. Kerr, CFA

Newsletter

April 28, 2023 – DJIA = 33,826 – S&P 500 = 4,135 – Nasdaq = 12,142

Wall Street Asks If The Glass Is Half Full

To some the glass is half full and to others it’s half empty. This quarrel between optimism and pessimism arises throughout our world. These mindset differences are growing wider and deeper in many areas of our culture.

The financial markets have long been a battleground of opposing opinions. In fact, Wall Street has assigned each side a mascot – the bull and bear. And while the fight is never ending, the 2023 episode is exceptional.

This year is unique on countless levels with economics and finance having their share of distinctive issues. For example, the bulls and bears disagree about the impact and longevity of the Federal Reserve’s policy of raising interest rates. There is broad optimism that the Fed will stop raising interest rates soon and then pivot to reducing rates and loosening monetary conditions.

The pessimists in the financial community believe the Fed will continue raising rates and then will be patient before any shift. They point to multiple speeches by Fed leaders and Chairman Powell that emphasize the need to reduce inflation.

Another related and critical topic dividing the bulls and bears is the economy. The bulls, counting on the tailwinds from a Fed swinging to interest rate cuts, are predicting an economic rebound and growth starting in the second half of 2023. Additionally, the recent stock market declines, they believe, have priced in all bad news and it’s time to click the “buy” button.

The ursin view is much different. Inverted yield curves have historically led to recessions. The record level of the current inversion suggests that the recession will be deep and long. Layoff announcements have become a regular occurrence and their impact has not been fully felt.

We’re in the middle of the 1st quarter earnings reports and the numbers, so far, are troubling. 258 companies within the S&P 500 have released results. The summation of these reports shows revenue growth of 4.9% year-over-year. Earnings have fallen 2.6% for this same period. Looking at the industry sectors, technology reported a 1.2% decline in revenues with a 12.8% drop in profits. The same data for the Nasdaq 100 index (46 companies reported) is worse. Sales have increased 4.4% while net income is down 6.9%.

The banking crisis is another glass half full-empty development. Wall Street bulls are confident that the failures of Silicon Valley Bank and Signature Bank are isolated events and that the Fed and other regulators have addressed the problems. With the system stabilized, banks will start financing housing and businesses.

The bears contend that the crisis is starting and that it will continue to grow. The increase in interest rates during the past 12 months has impaired the loans that banks have on their books. The value of a low interest rate mortgage that was done years ago has plunged given the current level of rates.

This is a large problem for many lenders and their balance sheets have been devastated. Of course, the Fed has initiated a new program that basically allows a bank to pretend that an underwater asset is worth its original value. They are lending to all banks based on fabricated numbers. This might work in the short term, but it doesn’t address the problem of the loss of value.

Opposing viewpoints drive the markets. A buyer sees value while a seller sees an opportunity for liquidity. The willingness of each party to transact at an agreed price is what makes markets. The capital markets of 2023 are facing widely differing views. Economic developments as well as geo-political and international problems will drive the markets. Ultimately the views of the bulls and bears will determine the path forward.

1st Quarter 2023 Recap – 2nd Quarter Influences

/0 Comments/in Financial Planning News /by jkerrIdes of March 2023, Banks Beware

/0 Comments/in Financial Planning News /by jkerr“Bad News is Good News”

/0 Comments/in Financial Planning News /by jkerrKerr Financial Group

Kildare Asset Mgt.

Jeffrey J. Kerr, CFA

Newsletter

February 3, 2023 – DJIA = 34,053 – S&P 500 = 4,179 – Nasdaq = 11,816

“Bad News is Good News”

Bad news is good news. This has become the rally cry of a lot of Wall Street bulls. The logic is that economic bad news will mean that the Federal Reserve will stop raising interest rates, reducing their balance sheet and other restrictive monetary machinations sooner.

Fortunately for the bulls, when it comes to bad news, they have had plenty of ammunition. Recessionary economic statistics, falling consumer confidence, widespread layoffs, and tumbling corporate profits are some examples. While many would apply common sense and conclude that these signals are a negative for the financial markets, the current investor attitude is that this will force the Fed to back off and then it is back to party time.

This mentality has helped stabilize the stock market in recent months after a horrible first half of 2022. It further assisted a strong stock market rally in January 2023. The Nasdaq Composite jumped 11% in January which is the best start to a year in over 20 years. The S&P 500 climbed 6.2% in the month.

At risk of raining on the bull’s parade, it might be useful to look past the intense emotional state of the capital markets. Taking a glance at the financial fundamentals, it shows an extremely overvalued condition. This may not matter in the short term, but it will likely be a headwind if it continues.

At the end of December 2022, the S&P 500 P/E (price to earnings ratio) stood at 28.7. To put this in perspective, the 50-year average of this number is 21. So, if there is any type of reversion to the mean, it is a bad binary outcome. The S&P 500’s price has to tumble while the earnings stay the same. Or the earnings number does a rocket launch which will reduce the multiple.

Unfortunately, recent earnings reports and the guidance for 2023 does not foretell any material increase in earnings. But if things like 0 days-to-expiration options (0DTE) and similar trading strategies continue to squeeze prices higher, maybe it buys enough time for the Fed to back off. This seems like a low probably outcome but so did an 11% monthly increase for the Nasdaq.

Trading Mechanics Get 2023 Stock Market Off To A Good Start

/0 Comments/in Financial Planning News /by jkerr“New Year, New Me”

/0 Comments/in Financial Planning News /by jkerr